Vietnam: Decree 182 on Investment Support Fund

Nghị định 182/2024/NĐ-CP về thành lập, quản lý và sử dụng Quỹ Hỗ trợ Đầu tư

KPMG Vietnam

17th January 2025

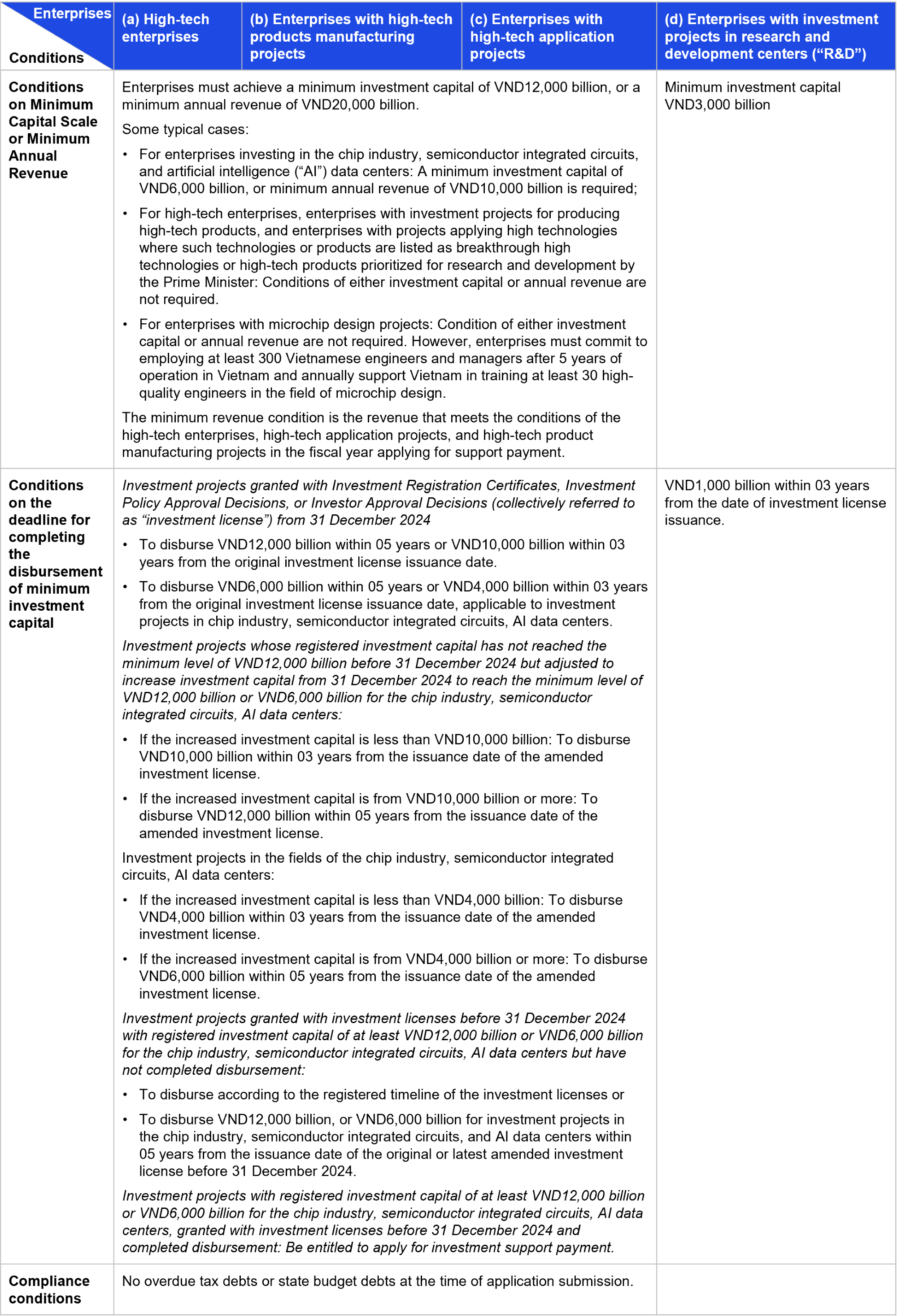

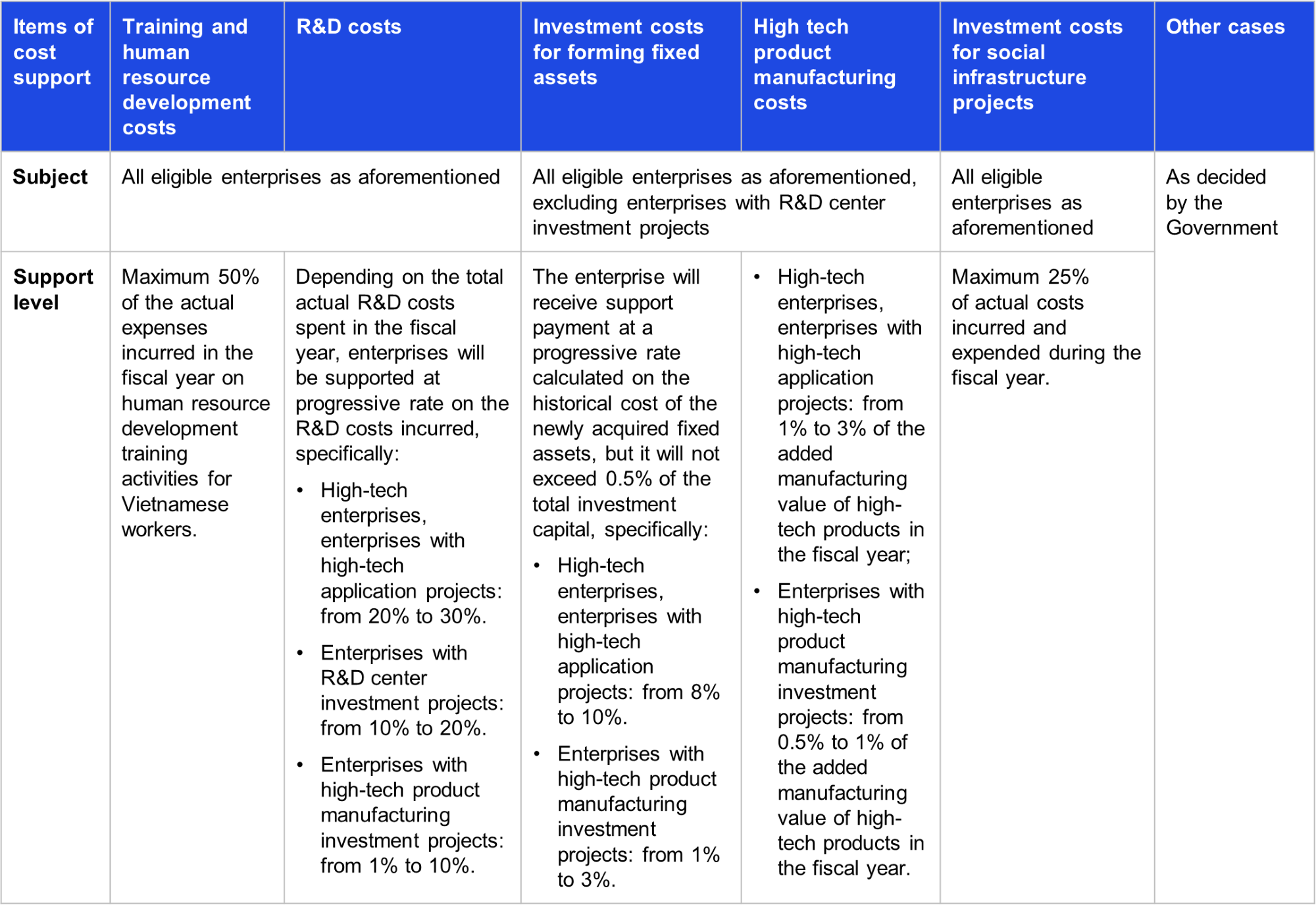

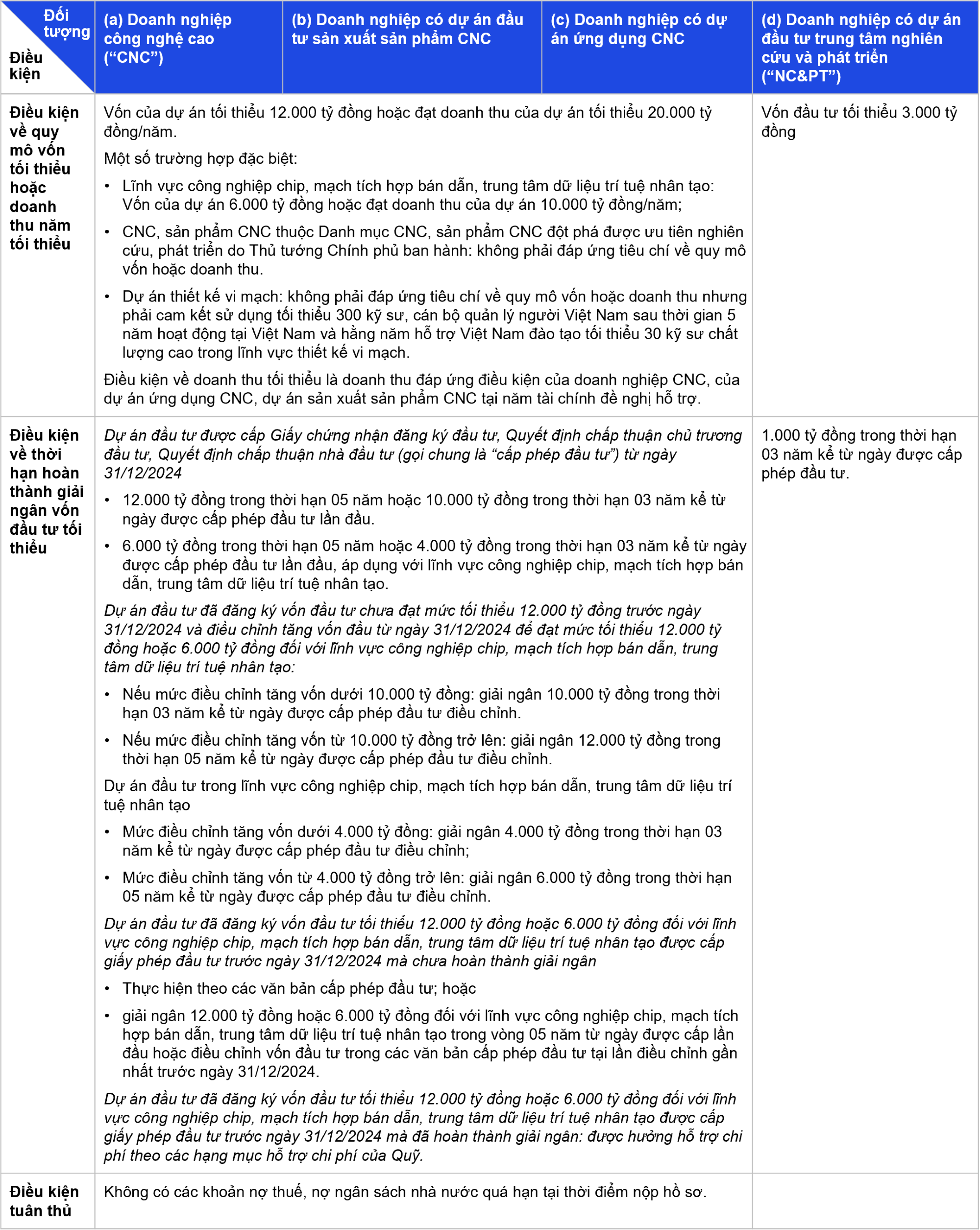

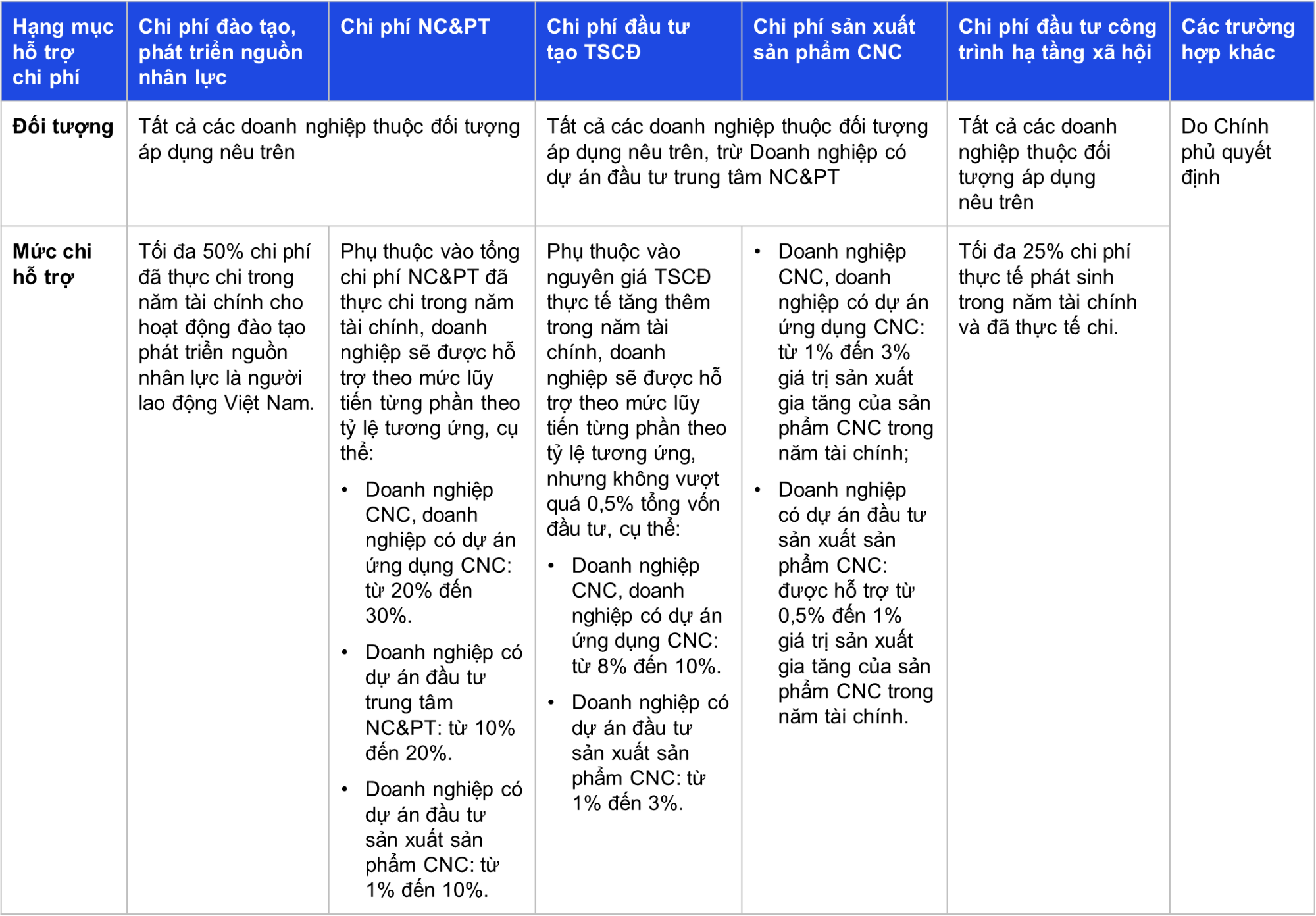

To aid in applying the Global Minimum Tax from 1 January 2024, the Government issued Decree 182 in December 2024 on the establishment, management, and use of the Investment Support Fund to stabilize the investment environment, encourage and attract strategic investors, and support enterprises in specific prioritized fields.

Please Login or Register for Free now to view all updates and articles

In addition to free-to-view updates and articles, you can also subscribe to the full Legal Centrix Vietnam Service including access to:

- Overview notes on the law

- Thousands of high quality translations of legislation covering all key business areas

- Legal and tax updates

- Articles on important legal and tax issues

- Weekly email alerts

- Sophisticated web platform and search

Legal Centrix is trusted by top law and accounting firms.

KPMG Vietnam

- Vietnam

- kpmg.com.vn

We Set Standard In The Industry

Global network with 197,263 people in 154 countries

️

Click here to view the author's profile

Author

-

KPMG Vietnam

Vietnam

Tags

Related Content

- No related content

Recent updates

- Decree 356/2025/ND-CP On Detailed Regulations On A Number Of Articles And Measures For Implementing The Law On Personal Data Protection

- Vietnam: Mediation in Intellectual Property disputes

- Vietnam: Recent Regulations On Auctioning Land Use Rights For Residential Land Allocation, Capital Contribution Activities in Credit Institutions, and Personal Data Protection

- Vietnam: Third-party funding in the resolution of investment-related disputes: A financial risk-reduction method for doing business with Europe

- Vietnam: Shareholders’ agreements indirectly recognized via beneficial ownership

- Vietnam: Electronic signatures in investment registration dossiers: Inevitability and practical challenges

A leading provider of legal and tax know-how and information for Asia.

Copyright © 1997 - 2026 Legal Centrix. All Rights Reserved Privacy Policy | Terms of Use